Where Property Outcomes Are Really Decided

Most property commentary focuses on the moment of purchase.

The price paid. The yield forecast. The long-term upside.

In practice, very few property outcomes are determined at that point.

They are decided later, during a much quieter and less discussed phase. The period after purchase, before stability is reached. This is what I refer to as the hold.

It is during the hold that behaviour changes, pressure builds, and outcomes diverge.

The misunderstood middle

After a property is purchased, most investors enter a period of cash flow pressure.

- Interest costs rise.

- Holding costs become clearer.

- Rental income grows slowly, if at all.

- External changes arrive without warning.

This is normal. It is not a failure of strategy. It is simply how property works.

What matters is how that pressure is managed.

Some investors stabilise and hold. Others are forced to exit earlier than planned. The difference between those two outcomes is rarely about optimism or long-term belief. It is about cash flow endurance.

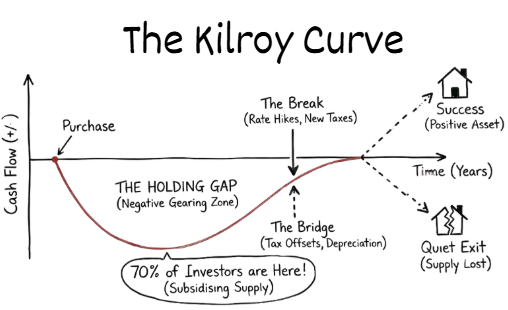

Introducing the Kilroy Curve

The Kilroy Curve illustrates this holding phase.

At purchase, cash flow typically deteriorates before it improves. This creates a holding gap, a period where costs exceed income and pressure accumulates.

During this phase, external shocks often arrive. Interest rate changes. New taxes. Insurance and maintenance increases. Each adds weight at the worst possible time.

For many investors, this is where decisions are forced.

Not because the asset is fundamentally flawed, but because it becomes too difficult to carry.

Why this matters beyond the individual investor

When an investor exits during the hold, a property often leaves the rental market.

- It may be sold to an owner-occupier.

- It may be redeveloped.

- It may be removed from the pool entirely.

When enough of these exits occur, rental supply tightens. Pressure shifts downstream. Rents rise. Access declines.

This is how housing outcomes are shaped quietly, one forced decision at a time.

Housing supply is not only about what gets built. It is about what survives the hold.

The false focus on purchase

Most advice still concentrates on buying well.

That matters, but it is incomplete.

The majority of risk sits between purchase and stability. Yet this period receives the least attention.

Very few investors fail because they misjudged the long-term potential of an asset. Many struggle because they underestimated how long they would need to carry it under pressure.

Reducing pressure changes behaviour

Anything that reduces pressure during the hold increases the likelihood of a positive outcome.

That does not mean eliminating risk. It means understanding where pressure builds and managing it deliberately.

- Cash flow clarity matters.

- Accurate construction cost recognition matters.

- Defensible depreciation decisions matter.

- Timing matters.

These are not aggressive strategies. They are stabilising ones.

They give investors time, and time changes behaviour.

A simple truth

Property does not fail at purchase.

It fails under pressure, during the hold, when decisions are no longer optional.

Understanding that period is the difference between assets that survive and assets that exit prematurely.

If housing outcomes are to improve, attention needs to move away from the moment of purchase and toward the reality of holding.

That is where outcomes are decided.

Frequently Asked Questions

Why is the holding period more important than the purchase?

A property is purchased once but held for years or decades. The cumulative impact of interest rates, tax law, holding costs, depreciation and vacancy across that holding period is far larger than any acquisition-day discount or premium. Most failed investments fail during the hold, not at the purchase.

What is the HOLD framework?

HOLD is a four-part diagnostic developed by Mark Kilroy assessing Holding costs, Optimisation, Liquidity and Demand. It is used to determine whether a property can continue to be held through changing conditions or whether structural pressure is building toward a forced exit.

Who should review the holding strategy of an existing property?

Any owner whose interest rate fix is rolling off, whose cash flow position has tightened, whose tax circumstances have changed, or who has held the asset for more than five years without reviewing the structure should reassess holdability against current conditions.

Explore further

Related commentary

Frameworks & tools

Republishing

You're welcome to republish this article in full or in part, provided it includes clear attribution to Mark Kilroy and a link back to the original at markkilroy.com.au.

For media enquiries, syndication requests, or to discuss republishing in print or digital publications, please get in touch.

The Kilroy Brief

Independent commentary on Australian housing, property, construction, taxation and investment, delivered directly to your inbox.